Who Loses the Tariff Wars: USA or China?

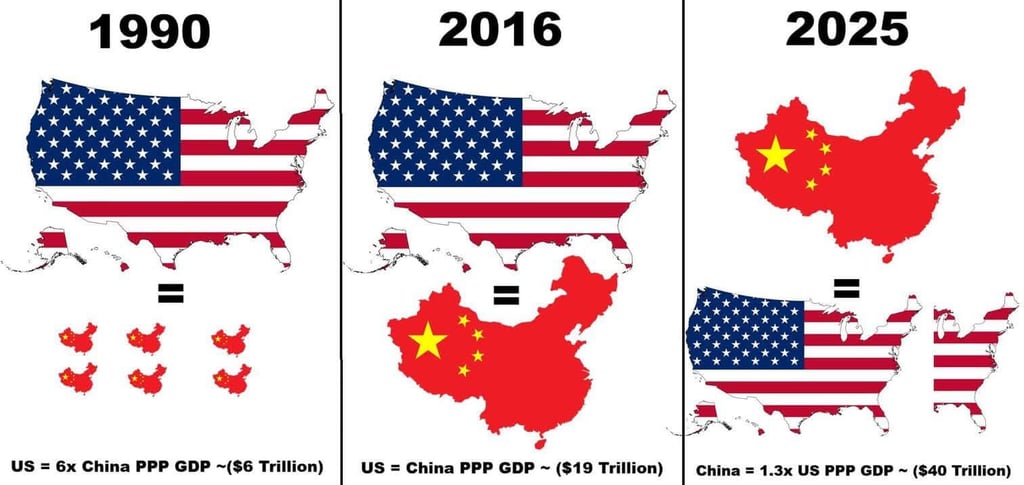

China may have a bigger GDP in terms of purchasing power (PPP)–$39.44 trillion versus the US's $30.34 trillion, but that doesn’t mean it holds the upper hand in the ongoing tariff wars. Here’s why the U.S.–China tariff war could hurt Beijing more.

GENERAL BUSINESS TOPICSGENERAL TOPICSCUSTOMER LOYALTYSOCIAL COMMENTARYSCIENCE & TECHNOLOGYINTELLIGENCENATIONAL SECURITY

Big GDP, Bigger Risk: Why China Has More to Lose in the Tariff War

The tariff war between the U.S. and China, especially under President Trump, has drawn global attention. But while much of the world focuses on the verbal sparring and retaliatory tariffs, a deeper question lingers: Who will be hurt more—China or the United States?

Some observers point to China’s impressive GDP in Purchasing Power Parity (PPP)—projected at $39.44 trillion in 2025, compared to $30.34 trillion for the U.S. They argue that this makes China more economically equipped to absorb the shocks of a prolonged trade war.

But that argument misses the mark.

PPP measures the value of goods and services within a country, adjusting for local prices—not for global trade muscle. And when it comes to trade wars, it’s not who looks bigger on paper that wins, but who has more control over international systems and fewer structural vulnerabilities.

Let’s break it down.

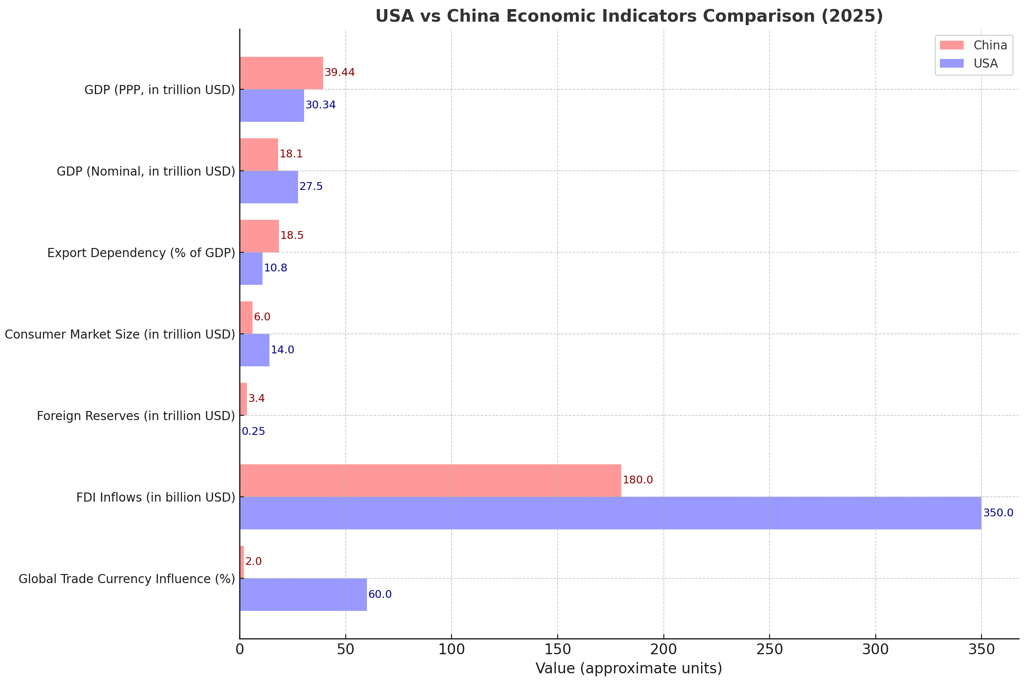

A comparative table and graph, showing the key economic indicators for China and the USA in 2025.

Can tariff wars hurt China more than the U.S., despite its larger PPP GDP?

Yes, and here’s why:

1. Export Dependence

China remains more reliant on exports than the U.S.

Though it's trying to build domestic consumption, exports still form a major chunk of its GDP.

The U.S., in contrast, runs a consumer-driven, service-heavy economy, with less vulnerability to trade disruptions.

2. Dollar Dominance

Most global trade happens in U.S. dollars, giving America a critical edge.

U.S. policymakers have greater monetary flexibility and control over global financial networks.

Chinese companies reliant on dollar transactions can face crippling restrictions during tariff escalations.

3. Supply Chain Fragility

China’s tech sector relies on high-end components from abroad.

The U.S. and allies like Japan and the Netherlands can restrict critical technologies, disrupting China's production capacity.

Even a larger domestic market can’t shield China from global supply chain disruptions.

4. Investor Confidence

Wall Street is still the world’s most trusted financial hub.

Trade tensions can trigger capital flight from China, weaken the yuan, and scare off foreign investment.

The U.S. can weather investor panic more easily thanks to stronger institutions and deep financial markets.

5. PPP ≠ Trade Power

PPP is great for measuring domestic well-being, not global economic influence.

Nominal GDP, where the U.S. still leads, reflects actual dollar-based capacity to engage in international trade, repay debts, and shape financial markets.

Bottom Line

China may look stronger in PPP terms, but that doesn’t translate into trade war resilience. The U.S. still has:

More control over global currency and financial systems

A larger consumer economy to cushion internal shocks

Greater international influence and investor trust

China has more to lose—and perhaps more reason to de-escalate.

When two elephants fight, the grass suffers. But one of these elephants is still heavier where it matters most.

COMMENTS: Comments are disabled for this post.

Get in touch

Nwankama Nwankama

Email is best (or, you can fill out the Contact form)

nwankama@nwankama.com

Home | About Me | Projects | Blog | Social Media | Contact Us